Back to Blog

Projected Impact of Agentic AI on the Australian Economy (2025–2030)

Generated by Triniti in Collaboration with ChatGPT Research

Executive Summary

Australia is on the cusp of a once-in-a-generation economic disruption driven by Agentic AI – autonomous AI systems capable of performing complex, decision-driven tasks. Over the next 2–5 years, accelerating AI adoption is expected to reshape the workforce, reduce wage incomes, and strain key economic sectors. Conservative estimates indicate a net shrinkage of ~11% in Australia’s job market (about 1.5 million fewer workers by 2030), concentrated in white-collar and administrative roles (1) . More pessimistic scenarios warn that up to one-third of Australian workers could face job displacement by 2030 if AI uptake is unchecked (2) . This wave of automation could erode annual salary expenditure by tens of billions of dollars – on the order of AUD $13B (moderate) up to $50B (severe) – with commensurate hits to income-tax, GST and other revenue bases. The ripple effects from lost jobs and incomes may dampen consumer spending (~60% of GDP) (3) , pressure the housing market, and tighten credit conditions, creating second-order impacts across retail, travel, hospitality, education, and other services. Socially, a rapid AI-driven workforce transition risks higher unemployment/underemployment, widening inequality, and psychological costs for displaced workers (loss of purpose, mental health challenges (4) ). Politically, these stresses could fuel populist sentiment, demands for safety nets like Universal Basic Income (UBI), and tests of government capacity to manage the upheaval.

On the positive side, Agentic AI promises significant productivity gains (up to +30% per employee in firms that fully integrate AI (5) ) and will create new tech-driven roles (e.g. an estimated 200,000 AI- specialist jobs by 2030 in Australia (6) ). However, these benefits will not fully offset the short-term dislocation in traditional sectors. This report provides a comprehensive analysis of quantitative forecasts (jobs at risk by industry, potential salary and tax losses) and an impact analysis of how these changes could cascade through the economy and society. It also includes illustrative visuals – workforce change charts, economic ripple diagrams, a timeline of disruption phases, and a systems map – to help stakeholders visualize the transformation. Finally, it offers policy recommendations to mitigate the downsides: from regulatory measures to slow or guide AI-driven disruption, to economic adaptations (like UBI or an “AI productivity tax”), to social infrastructure reforms (for reskilling, mental health, and community support). The goal is to support Australian decision-makers in understanding and preparing for the agentic AI revolution, ensuring that the coming productivity gains do not come at the cost of societal well-being. Immediate proactive planning is critical – the window to balance innovation with inclusion is now.

Quantitative Forecasts and Data

Job Displacement Forecasts by Sector: Agentic AI will unevenly impact industries, hitting roles with high routine or data-processing content the hardest. Table 1 summarizes projected job displacement in five vulnerable sectors by 2030, based on current employment levels and automation studies:

Table 1: Estimated Australian job displacement in key sectors by 2030 (figures are illustrative ranges). Finance and insurance face major automation of transactional and documentation tasks; one study finds up to 1,000,000 finance/accounting/procurement jobs nationally could be eliminated by automation by 2030 (8) . Administrative/clerical roles are most at risk – by one estimate 63% of “cubicle jobs” (routine office work) will be automated by 2030 12 . Professional services (consulting, law, accounting) see moderate task automation (20–30% of tasks 10 11 ), limiting outright job loss to perhaps ~10–20%. Crucially, even when jobs aren’t fully eliminated, AI will transform roles and reduce headcount growth. For example, in legal services, AI can handle document review and research, allowing one lawyer to accomplish work that used to require several – McKinsey estimated ~22% of a lawyer’s tasks and 35% of a law clerk’s tasks could be automated 10 . Consulting similarly may not see mass layoffs, but ~27% of consultant tasks can be offloaded to AI 11 (data analysis, slide generation, etc.), which will reduce demand for junior consultants and support staff.

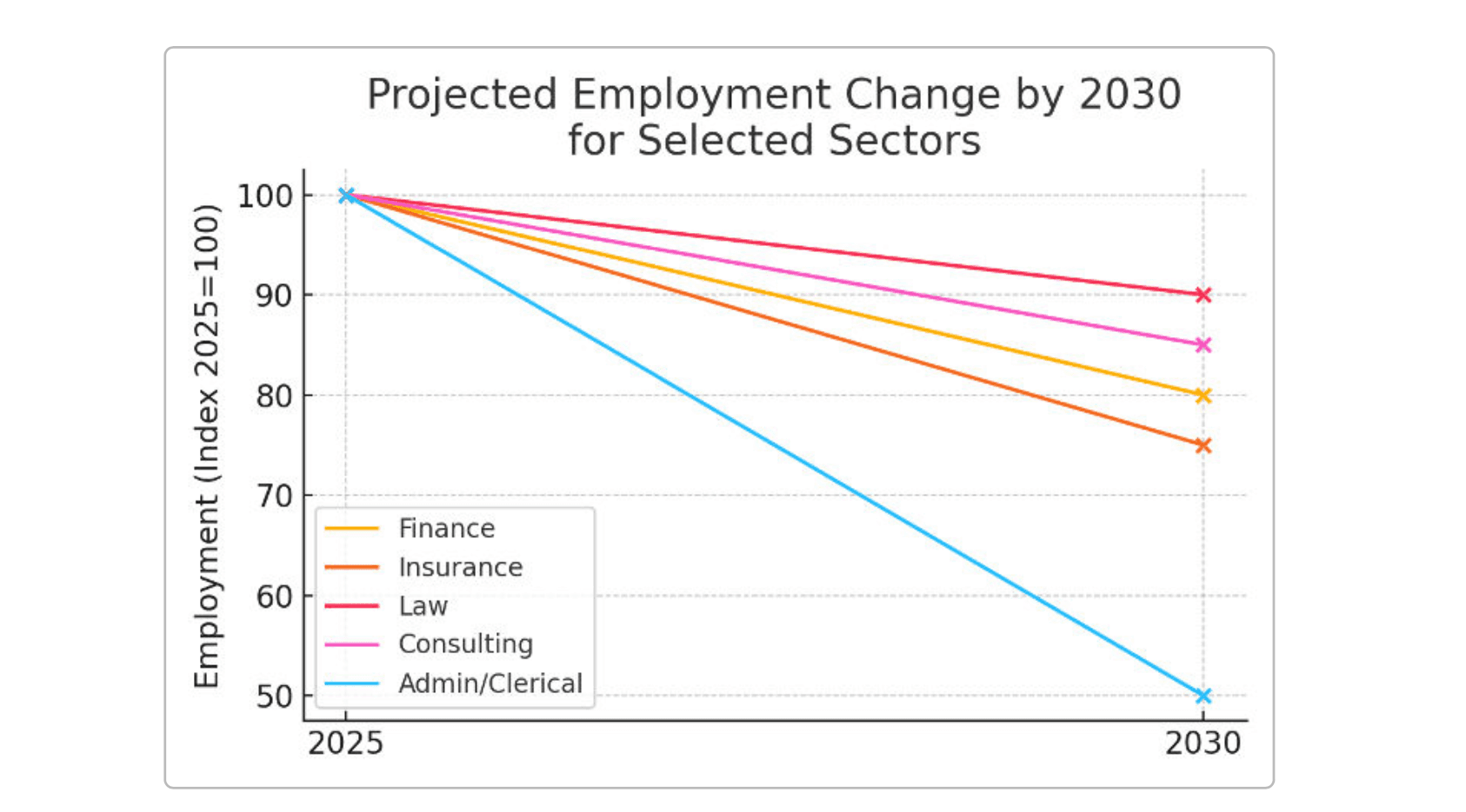

Figure 1: Projected decline in employment (index, 2025=100) for select sectors by 2030. Finance (orange) and insurance (brown) roles are expected to shrink significantly as AI automates routine financial analysis,2

reporting, and customer service. Administrative/clerical jobs (blue line) see the steepest drop – potentially halved by 2030 – reflecting the high automaton potential of repetitive office tasks 12 . By contrast, law (red) and consulting (pink) experience smaller declines (~10–20%), as these fields retain a larger need for human judgment, creative problem-solving, and interpersonal skills. (Projection based on sources and automation potential data 8 10 ).

Salary Expenditure Contraction: The displacement of tens of thousands of mostly mid-skilled, white- collar jobs will translate into a substantial contraction in aggregate salaries paid. In 2024, Australians earned about $1.0 trillion in wages nationally (roughly, given ~14.5 million employed and an average annual wage around $70k). The elimination or downgrading of 1–1.5 million jobs could remove on the order of $30–$90 billion in annual wages by 2030 (before accounting for new jobs created). Even factoring in some redeployment and new “AI economy” roles, net lost wages are likely in the tens of billions. For instance, if ~10% of jobs (around 1.3 million) see lower wages or vanish, at an average ~$50k–$60k per affected job (many impacted roles are mid-level), that’s roughly $13–$20B less in yearly payroll. In a more severe scenario (25% jobs affected, e.g. ~3 million workers with reduced earnings), the wage bill could shrink by $50B or more per year. These rough estimates align with firm-level projections: HR executives foresee a 19% reduction in labor costs once AI agents are fully implemented (about $11k savings per employee on average) 5 . By 2030, Australia’s total wages paid could be 5–10% lower than they would be without AI disruption, a hit that represents lost spending power in the economy. Moreover, wage growth for remaining jobs might be suppressed as AI-driven productivity caps demand for labor. In short, household incomes will take a significant hit, especially in the affected industries.

Such a drop in salaries will have multiplicative effects across the economy. Every dollar of wage income typically circulates through consumption and investment (“income multiplier”). A contraction of, say, $50B in wages doesn’t just remove $50B of demand – it can reduce GDP by closer to $75–$100B once indirect effects are included, as businesses earn less and cut their own spending. Figure 2 illustrates this ripple effect qualitatively.

Tax Base Erosion: A shrinking wage pool directly erodes government revenues. The Australian Commonwealth budget is heavily reliant on personal income tax (PAYE) – which brought in ~45% of tax revenues pre-AI. If annual wages drop by $50B, and assuming an average effective tax rate of ~25%, that’s roughly $12.5B less income tax collected per year. Even a modest $20B decline in wages could mean ~$5B less PAYE receipts. Additionally, GST (goods and services tax) will suffer as unemployed or income-hit households cut spending – GST takes 10% of consumption, so a drop of (for example) $30B in consumption would reduce GST revenue by $3B. Company profits taxes may also decline if consumer demand falters and businesses see lower earnings. State governments would feel the pinch through lower stamp duty (if housing activity slows due to job insecurity) and potentially lower payroll tax if employment falls. Superannuation contributions (currently 11% of wages) would fall in absolute terms as well – impacting the long-term retirement savings pool (and by extension, future investment funds). In summary, an AI-induced downturn in employment could push Australia’s tax base materially lower, complicating budget planning. Governments may face difficult choices as social welfare outlays (unemployment benefits, retraining programs) rise while tax inflows decline 13 . Without policy action, there is a risk of a widening fiscal gap: one analysis warns that sustained high unemployment from AI could force higher taxes elsewhere or new revenue measures 13 .

To illustrate, consumer spending accounts for ~60% of Australian GDP 3 . Mass unemployment or wage loss means households tighten their belts, shrinking consumption and GST. Meanwhile, higher unemployment raises welfare costs (JobSeeker, etc.) and reduces superannuation inflows (since super is a fixed share of wages). Figure 2 below conceptually maps these cascading economic effects:

Figure 2: “Ripple Effect” of salary contraction on the broader economy. The flowchart shows how AI-driven job losses lead to a chain reaction: As AI adoption replaces workers, it causes job displacement and lower aggregate wages. Reduced household income in turn suppresses consumption and consumer demand, which hits business revenues. Businesses facing declining sales often respond with cost- cutting and further layoffs, feeding back into job losses. Lower consumption also means lower GST collection, and reduced wages mean less PAYE income tax – contributing to a shrinking tax base that can strain government budgets. Other second-order effects include housing market stress (as incomes drop, many struggle with mortgages) and credit tightening (banks become wary as defaults rise, making loans harder to get). This systemic feedback loop can amplify an initial AI shock into a broader economic downturn if unmitigated.

Impact Analysis

Agentic AI’s economic impact will extend far beyond the immediate loss of certain jobs or wage income. The following sections analyze key areas of impact and how they interconnect, from the labor market to social and political domains.

Employment and Underemployment

Unemployment Surge: As AI automates millions of tasks, Australia could see a sharp rise in unemployment absent new job creation. The official unemployment rate (around 4% in 2024) could climb into the high single digits or low double digits by late-decade if displacement outpaces job creation. An analysis by Forrester predicts Australia’s labor market will shrink by 11% (net) by 2030 1 – effectively taking unemployment to levels not seen since the early 1990s recession. In a worst-case scenario, one in three workers might lose jobs (at least temporarily) due to AI by 2030 2 . Even those keeping jobs may face wage pressure as AI alternatives cap salary growth. Certain occupations (especially in finance and administrative support) could become scarce for human workers, leading to localized unemployment spikes in those fields.

Underemployment and Gig Transition: A subtler effect may be underemployment – people still working but fewer hours or in lower-paying gigs than they prefer. Companies might shift workers to part-time or consulting roles as AI takes over core duties. Forrester’s study noted that some displaced roleswillre-emergeaspartofthe“gigeconomy”orfreelancework 14 .Ratherthanbeingfullyjobless, many might string together short-term contracts or reduced-hour roles. This can mask true joblessness but results in incomes below full-time level. Australia already had underemployment challenges; the AI disruption could exacerbate this, creating a large class of workers who are “partially employed” or doing piecemeal work. MacroEconomic commentators warn that without intervention,underemployment could become the new normal (“endemic”) as firms utilize AI and only hire humans for residual tasks or on-demand needs 15 . In sum, job insecurity is likely to grow – stable long-term employment may give way to more fragmented career paths for many. Worker anxiety about the future of their jobs is already evident, with surveys showing growing AI-related job insecurity in Australia 16 .

On the positive side, new job opportunities will emerge – particularly in the AI sector itself (Australia could gain ~200k AI specialist jobs by 2030 6 ) and in areas requiring human skills complementary to AI (e.g. trainers, ethicists, or creative roles). There will also be redeployment: many workers will transition into new roles alongside AI. A global HR survey found 89% of companies expect to reassign employees to new roles rather than lay them off, as AI agents roll out 17 . However, these transitions require significant retraining, and not all displaced workers will smoothly find new positions by 2030.

The net outcome for the latter 2020s is likely a higher unemployment rate and a spike in retraining needs, even as productivity rises.

Housing Market Pressure and Mortgage Stress

The housing market, a cornerstone of Australian wealth, will not be immune to an AI-driven shock. Widespread job losses or wage cuts would reduce the ability of households to service mortgages, potentially leading to a rise in mortgage delinquencies and forced sales. Australia enters this period with record-high household leverage – as of Q4 2024, household debt was about 182% of disposable income (mostly mortgages) 18 . The median mortgage payment already consumes ~50% of household income for new buyers 19 . This means even a moderate drop in income (or loss of one earner in a household) can push many families into financial distress. If AI disruption causes unemployment to climb, mortgage arrears and defaults could increase, putting downward pressure on house prices. A large pool of distressed sales can soften the property market, eroding home equity for millions. This “negative wealth effect” (people feeling poorer as home values fall) would further depress consumer spending 20 .

Conversely, an AI-induced downturn would likely prompt policy responses that affect housing: the Reserve Bank might slash interest rates to stimulate the economy, as some analysts predict (e.g. multiple rate cuts expected in 2025 amidst softening conditions) 21 . Lower interest rates would normally support housing demand. However, if banks simultaneously become more risk-averse, credit availability could tighten – lenders may raise credit standards, requiring bigger deposits or proof of secure employment (which is harder to come by in a turbulent job market). This credit tightening could offset the benefit of rate cuts. We might see a paradox of cheap money that few can borrow due to stringent lending criteria.

The net effect on the housing market could be a stagnation or modest decline in prices in the late 2020s, especially in areas with high exposure to affected industries (e.g. inner-city markets heavy with finance and IT workers might see reduced demand). Mortgage stress (households spending >30–40% of income on repayments) could become more widespread in the interim. If unemployment becomes “endemic” as a result of AI (in the worst case) 22 , the traditional Australian reliance on rising property values to boost consumer confidence may falter. Policymakers will then face pressure to intervene (for example, through mortgage relief programs or public housing expansion) to prevent a broader housing bust. Housing outcomes will depend on how quickly displaced workers find new income sources – a smoother transition means housing impact is contained, but a rocky transition means Australia’s highly- indebted households could be a flashpoint of economic pain.

Lending and Credit Market Tightening

Closely tied to housing and business activity is the finance/credit sector. A surge in unemployment and business closures triggered by AI would likely make banks and lenders more cautious. Higher default risks (on both mortgages and business loans) lead to tighter credit conditions – lenders may restrict new loans, increase interest spreads, or demand more collateral. Access to credit for homebuyers, small businesses, and even larger firms could contract just when the economy needs it most. This can create a credit crunch that further reinforces the downturn (less credit -> less investment and consumption -> more job cuts, and so on).However, there is a countervailing factor: AI adoption itself will greatly benefit the financial sector’s efficiency (e.g. AI for credit scoring, risk assessment, and cost reduction in banks). Banks may enjoy higher productivity and lower operating costs thanks to AI, which could boost their profitability in the short term. The danger is if they achieve those gains by dramatically cutting their workforce (Australian banks and insurers employ hundreds of thousands; many roles like loan processing, customer service, compliance checking are ripe for AI). If a million finance and accounting jobs are automated away nationally by 2030 8 , banks will save on wages but also contribute to the very unemployment that undermines their customer base.

In effect, the financial system could face stress from two sides: operational disruption (as they restructure workforce and implement AI) and market disruption (as economy-wide defaults rise). Regulators (APRA, RBA) will likely keep a close eye to ensure bank stability. They have indicated household debt is high but systemically banks have buffers 23 18 . In an AI-induced recession, we might expect regulatory interventions such as loosened lending criteria for small businesses (to encourage investment), or government loan guarantees for certain sectors, to keep credit flowing.

One probable scenario is a period of low interest rates (even near 0%) coinciding with high risk premiums. Indeed, if AI causes a deflationary effect on wages and prices, central banks will cut rates aggressively 22 . But private lenders, wary of defaults, might not pass on all that cheap money to end borrowers. So, interest rates “on paper” could be low, yet credit is effectively rationed to only the safest bets. Businesses that do borrow may find banks insisting on strong financials or personal guarantees, which many struggling owners cannot provide. This could particularly squeeze small and medium enterprises (SMEs) and startups, potentially dampening the formation of new businesses that could otherwise absorb displaced workers.

In summary, unless carefully managed, AI disruption could lead to a paradox in the credit market: easy money policy but tight lending practice. The result would be slower recovery, as lack of credit stymies entrepreneurship and consumer purchases (like homes, cars). The government might need to step in with targeted credit programs or pressure banks to maintain reasonable lending growth even amid higher unemployment. The health of Australia’s banking sector itself will be critical – if banks remain profitable and well-capitalized (perhaps even benefiting from AI efficiency), they can be part of the solution; if they hit a crisis, they become part of the problem. Prudently, Australia enters this era with a strong banking system and regulatory oversight, which is a stabilizing advantage compared to some countries.

Downstream Industry Impacts (Retail, Travel, Education, Hospitality, Insurance, Services)

When a significant share of the population has less money to spend (or is worried about their job security), discretionary spending is one of the first things to be cut. This spells trouble for industries reliant on consumer confidence and disposable income:

Retail: Everything from department stores to online retail could see reduced sales. Big-ticket items (electronics, vehicles, appliances) are often deferred during uncertain times. We may see a drop in retail employment beyond the direct AI effects (which are also non-trivial: retail is automating via self-checkouts and AI inventory management). So retail faces a double hit: fewer shoppers and more automation. Large retail chains might accelerate use of AI for supply chain and customer service (chatbot-based sales assistance, etc.), further reducing staffing needs. Small retailers could struggle to stay afloat with lower foot traffic. For example, AI in customer service (chatbots, virtual assistants) is already reducing the need for human call-centre operators 24 , and automated checkout systems reduce cashier jobs 25 . If consumer spending stalls, expect store closures and consolidation in the retail sector.

Hospitality & Restaurants: Dining out, entertainment, and travel are classic discretionary spends. Restaurants may see fewer patrons and smaller spends (e.g. less frequent dining, no dessert or wine to save money). The hospitality industry might respond by cutting hours or staff, and using technology (like tablet ordering, robotic kitchen assistants) to trim labor costs. Fast-food chains in particular can lean on AI and robotics for food prep and service, meaning job losses among waitstaff and kitchen hands in addition to reduced demand. Travel and tourism could be severely impacted if joblessness rises domestically and if global trends mirror Australia (since inbound tourism would also suffer). Households facing mortgage stress and job uncertainty will likely postpone holidays, hitting airlines, hotels, and tour operators. We could see discounting in travel, but many may simply not travel at all, causing a slump similar to a recessionary environment for that sector.

Education: The education sector might experience complex effects. On one hand, during periods of higher unemployment, more people might pursue further education or re-skilling, boosting enrollments in universities, TAFEs, or coding bootcamps. Indeed, government and industry reskilling programs (if funded) could channel displaced workers into training, providing a positive demand shock for education services. On the other hand, private education and training providers rely on people (or employers) being able to pay – tight budgets could mean lower enrollment in fee-paying courses (e.g. international student numbers could fall if the global economy slows, domestic students might defer costly postgraduate study). Additionally, AI itself is entering education: AI tutors, automated grading, and personalized learning systems could eventually reduce the need for some teaching and administrative staff. For the 2025– 2030 horizon, education is listed as one of the sectors facing rapid disruption from Gen AI 9 . Universities may need fewer tutors if AI can help mark papers or answer student queries. Overall, education and training are critical for adapting to AI, so one hopes any dip in private spending is offset by public investment in upskilling the workforce.

Travel & Tourism: As noted, travel is highly sensitive to economic confidence. In addition to fewer leisure travelers, business travel might decline for structural reasons: with advanced AI and collaboration tools, companies may cut back on flying staff around, using virtual meetings or AI-driven analytics instead. Australia’s airlines, already challenged by the pandemic, could face a prolonged period of weaker demand. Regions dependent on tourism (coastal Queensland, parts of NSW etc.) might suffer higher local unemployment. The timeline of disruption (Figure 3) suggests the late 2020s could be a tough period for travel until the economy finds a new equilibrium.

Insurance & Financial Services: Beyond the direct job losses in insurance companies (from AI automation of underwriting, claims processing, etc.), there’s a second-order impact: if people buy fewer cars (or switch to cheaper ones), auto insurance revenue falls; if home values stagnate or people downsize, home insurance growth slows; life insurance and superannuation contributions may drop if incomes fall. Also, with more people feeling financially strained, some may let optional insurance policies lapse to save money, impacting industry revenues. Paradoxically, times of stress often increase demand for certain insurance (like income protection), but if too many claims come at once (e.g. a wave of income protection claims due to mass layoffs), insurers could face payouts that hurt their profitability. The insurance sector will need to manage AI both as a tool and a risk factor–using AI to cut costs and detect fraud 26 , but ensuring they maintain a broad customer base in a more economically polarized society.

General Services: Many service industries (from personal services like salons and gyms, to professional services like design agencies) will feel the downstream pinch. Consumers will prioritize essentials; businesses will trim service contracts if their revenues fall. For example, a consulting firm may see clients cancel projects – which then loops back to fewer consulting jobs. The multiplier effect of lost jobs thus spreads the pain to virtually all corners of the economy. Even sectors not directly automated by AI (like healthcare or construction) could experience slower growth if public and private funding is constrained.

In aggregate, these downstream impacts could mimic a classic recession: lower retail sales, empty hotel rooms, quieter restaurants, and businesses across the board cutting costs. The difference is that this downturn would be structurally driven (by technological change) rather than a typical cyclical or financial shock, meaning the recovery might not simply restore the previous status quo. Instead, consumer behavior may reset to a new normal. For instance, if AI drives long-term unemployment up, we could see a permanent reduction in consumption and a need for new industries or public-sector job programs to fill the void.

It’s worth noting that not all impacts are negative: AI itself will create new efficiencies and possibly lower the cost of goods and services, which could help consumers. For example, automation in retail and food service might make it cheaper to operate, potentially passing some savings to consumers (e.g. cheaper fast food due to robot cooks). These savings might modestly boost consumption of those cheap goods. However, the worry is that any such gains are overshadowed by the larger effect of people simply having less income or being too anxious to spend. The balance of these forces (productivity gains, price reductions vs. income losses, confidence drops) will determine how severe the net downstream impacts are. Current indicators (surveys of Australians) suggest caution: over half of Australian workers are already expecting significant change in their jobs from AI and many are saving more in preparation 16 , which in itself reduces short-term spending.

Social Consequences (Mental Health, Identity, Inequality)

The rapid upheaval in the job market is not just an economic story – it’s fundamentally a social one. Work is deeply tied to Australians’ sense of identity, purpose, and community. Large-scale displacement by AI could therefore trigger social consequences on multiple fronts:

Mental Health and Wellbeing: A sudden loss of one’s job or profession can be psychologically devastating. Workers facing unemployment due to automation often experience financial hardship, reduced self-esteem, and a diminished sense of purpose 4 . The term “techno- unemployment” has been linked to anxiety and depression as individuals struggle to retrain or find where they fit in a transformed economy 27 . We may see a spike in mental health issues, including anxiety disorders, depression, and substance abuse, particularly in regions or industries hit hard by AI layoffs. Even those who keep their jobs might face intensified stress: working alongside AI can impose new pressures (needing to continuously upskill, or meet higher productivity benchmarks set by AI-enhanced peers) leading to burnout 28 . Mental health services could see increased demand at a time when government budgets are strained, making access to care a challenge. Ensuring psychological support for displaced workers (counseling, community engagement, etc.) will be a major social task.

Identity and Societal Role: For many, their career is a key part of their identity – e.g. “I am a lawyer/accountant/admin and proud of the work I do.” The AI disruption threatens to uproot these identities. A mid-career professional who trained for decades may feel profoundly lost if their role is diminished by an AI system. This can lead to a societal phenomenon some have termed the rise of the “useless class” – individuals who feel economically and socially unnecessary, which is a recipe for alienation and social fragmentation 29 . Australia values the ethos of giving everyone a “fair go” and the dignity of work; if AI undermines that, we might need new ways for people to derive meaning (such as through community, arts, volunteerism, or other non-work avenues). Otherwise, a portion of the population could become disenfranchised not just financially but emotionally.

Inequality Widening: Without intervention, Agentic AI could significantly widen economic inequality. Those who own the AI technologies or have the high-level skills to complement AI will capture most of the gains, while many others lose income. The Sogeti analysis noted the concentration of wealth and power in the hands of AI tech owners could exacerbate socio- economic inequalities 4 . We could see a greater divide between a wealthy tech-savvy minority and a majority with stagnating or falling incomes. Australia already grapples with inequality (the Gini coefficient has been fairly stable but slightly rising in recent decades); an AI shock could push it higher, reversing any recent wage gains at the lower end. Regional inequality may also grow: tech and AI jobs cluster in major cities, whereas job losses (e.g. in admin support or back-office finance) might be nation-wide, including smaller cities that host processing centers or call centers. If, for instance, Sydney’s fintech firms thrive with AI while a regional town loses a big insurance back-office to automation, the gap between metro and regional fortunes grows. Inequality can breed resentment, crime, and reduced overall wellbeing.

Social Cohesion and Community Impact: High unemployment and underemployment can lead to erosion of social cohesion. Communities built around certain industries (e.g. a city with many public servants or bank offices) might see population outflows when jobs vanish, leading to urban decay in some areas. Those who remain may feel a loss of community pride and increased social ills. Crime rates could potentially rise if poverty and desperation grow (though this is a complex relationship). Trust in institutions might decline – people who feel left behind might blame government or business leaders for their plight. We’ve seen analogous patterns in regions affected by deindustrialization (like manufacturing towns in the 1990s): increases in family breakdown, drug use, and general despair. It’s critical to note these outcomes are not inevitable – proactive community support and re-investment can mitigate them – but they are real risks if AI disruption is unmanaged.

On the flip side, society might also adjust in some positive ways. With less work to do, people could have more leisure time (if supported financially), potentially leading to a cultural shift valuing pursuits outside of work. There’s a scenario where AI frees people from drudgery and allows more time with family or creative projects – but achieving this without exacerbating inequality requires intentional policy (like shorter work weeks or universal income). Absent such measures, the social consequences sketched above are a serious concern.

In summary, the social fabric will be tested. Australia may need to mount a response akin to past transitions (like the move from manufacturing to services) but at a faster pace. Investment in mental health services, community retraining centers, and narratives that value people beyond their job title will be important. The human side of the AI revolution must not be overlooked, as ultimately economic transformations are lived and felt by people in their daily lives.

Political Consequences (Populism, Policy Experiments, Governance Strain)

The economic and social upheavals brought on by agentic AI will inevitably become political issues. We can anticipate several possible political consequences:

Rise of Populism and Political Fractures: Historically, when large segments of the population feel economically left behind or insecure, they become fertile ground for populist movements and anti-establishment politics. Australia could see increased support for fringe or populist parties that promise simple solutions (e.g. curbing immigration, protectionism, or even “banning AI” outright) or that channel people’s anger toward elites. If inequality grows and unemployment remains high, mainstream parties (Labor and Coalition) might face pressure from new movements – for instance, calls to “put Aussie jobs first” which could manifest in opposition to global tech firms or trade. This could complicate Australia’s generally pro-trade, pro-investment stance. We might also see greater polarization in public discourse, with technology becoming a wedge issue (some framing AI as an evil to be stopped, others as an opportunity). The challenge for political leaders will be to address legitimate grievances without resorting to counterproductive populist measures. Failure to address the displacement could indeed fuel unrest: unemployment shocks have historically been linked to civil unrest and extreme politics, and Australia would not be immune if the social safety nets fail to catch people.

Demands for UBI and Welfare Expansion: One concrete policy idea that may gain traction is Universal Basic Income (UBI) – a guaranteed income floor for all citizens. As people witness AI taking jobs, the idea of decoupling livelihood from employment might shift from academic debate to political mainstream. There could be trials or pilot programs of UBI in certain regions or among certain groups (as has been piloted in some countries) to gauge its effectiveness in alleviating poverty and supporting consumption. Already, thought leaders globally have floated UBI in the context of AI; Australia’s unions and social groups might push for at least a serious study or small-scale implementation. In addition to UBI, expect debate around expanding unemployment benefits, wage subsidies, or public job guarantees. The social policy response will be a hot topic: e.g., “Should the government provide a living stipend to those displaced by AI? For how long? Universal vs targeted?” Politicians will need to grapple with these questions. We might also see the revival of ideas like a “Robot tax” – a tax on companies that replace workers with AI, to fund the safety net. While such a tax doesn’t exist in Australia yet, it’s been discussed internationally (South Korea has a form of it, the EU debated it, etc.), and could enter Australian policy conversations as a way to redistribute AI gains and slow down purely profit-driven automation.

Regulatory Action on AI: To address public concern, the government may take a more interventionist stance in regulating AI deployment in the labor market. Already a Senate Select Committee on AI recommended worker-centric regulation to prevent companies from using AI to erode wages and conditions 30 . We can expect new laws or regulations requiring, for example, consultation with employees before implementing AI systems that could cause redundancies, or perhaps requiring large employers to provide retraining or severance for AI- displaced workers. Government might also strengthen antitrust scrutiny on big tech companies in AI (to prevent monopolies that could have outsized labor impacts) – essentially guardrails to ensure the AI revolution doesn’t become a free-for-all at workers’ expense. The political appetite for such regulation will depend on how severe the disruption is; if unemployment is spiking, politicians will be forced to act (“AI impact” could become as salient as issues like climate or healthcare). On the flip side, Australia also won’t want to stifle innovation – so regulators will walk a tightrope, trying to slow the most harmful aspects of disruption without crippling the nation’s productivity gains or international competitiveness.

Governance and Fiscal Strain: Politically, managing this transition will put government institutions under strain. Unemployment insurance systems, retraining programs, and possibly public works/job creation schemes would need rapid scaling, demanding efficient bureaucracy. If tax revenues fall sharply (as discussed), governments might face budget crises, forced to either cut other services or increase borrowing. High public debt or unpopular tax hikes could result, becoming political liabilities. There’s also a risk of intergovernmental tension – federal vs state governments might clash on who funds what (e.g. states handle TAFEs and some job training, federal handles welfare – coordination will be critical). Public pressure might also rise on unrelated policies, as people conflate their economic frustrations with other issues. Essentially, the government’s capacity to respond decisively and fairly will be tested. If they succeed, social trust in institutions might even grow; if they fumble, it could lead to disillusionment and instability in the political landscape.

Social Unrest: In a worst-case scenario, prolonged mass unemployment and inequality could lead to protests or unrest. This is not a given – Australia has strong institutions and typically peaceful civic discourse – but one cannot ignore the possibility if enough people feel desperate. For example, imagine youth unemployment surging and a generation feeling “robbed” of opportunities by AI; that could spill into the streets in the form of demonstrations or support for disruptive political candidates. The government might preempt this by involving citizens in the transition (e.g. deliberative forums on AI policy, including worker voices, as unions are already insisting on 31 ). Keeping people heard and engaged can mitigate unrest.

In summary, the political sphere will be deeply engaged by the AI economic transition. We will likely see a new wave of policy innovation (or at least experimentation) in Australia, as it seeks to adapt capitalism to an era where not everyone’s labor is needed in the same way. Ideas once considered fringe – be it UBI, robot taxes, or government job guarantees – may enter the policy mainstream. How Australia’s democracy handles this will shape not just our economy but the very social contract. The hope is that proactive, inclusive policy-making can channel the disruptive energy of AI into a force for positive renewal (e.g. more leisure, new industries, stronger safety nets), rather than a cause of division. Much will depend on decisions made in the next few years, before the disruption fully peaks.

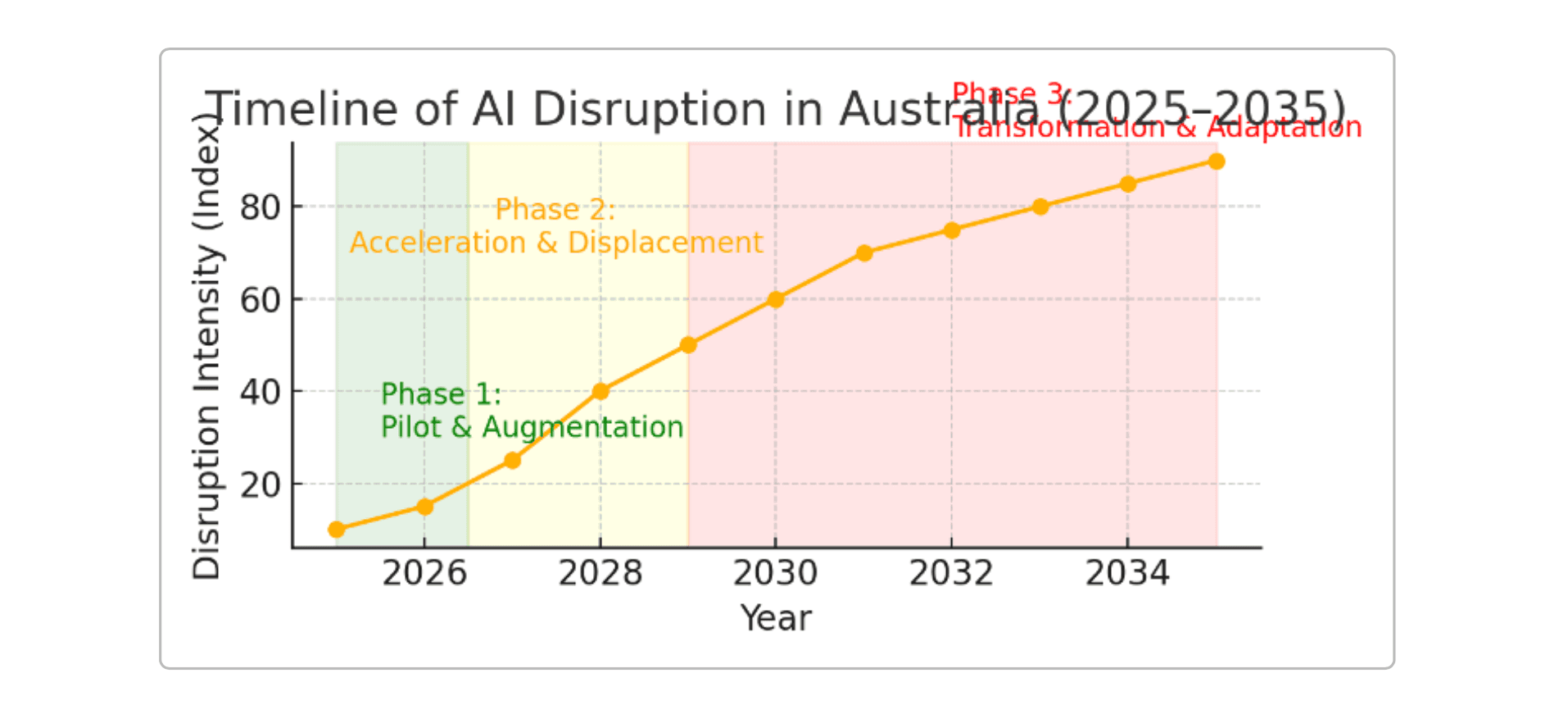

Figure 3: Timeline of anticipated AI disruption phases in Australia (2025–2035). Phase 1 (2025–2026): Pilot & Augmentation – Early adoption of agentic AI in workplaces leads to pilot programs and humans working alongside AI for the first time at scale. Productivity begins rising, but job impacts are modest and localized. Phase 2 (2027–2029): Acceleration & Displacement – AI use surges (many organizations move from 15% to >60% adoption 32 ), bringing a rapid productivity jump but also widespread job restructuring. This is the peak period of displacement: layoffs in admin, finance, and support roles accelerate, and unemployment climbs. Social and economic strains become evident (governments scramble with policy responses). Phase 3 (2030–2035): Transformation & Adaptation – Having absorbed the shock, the economy begins to stabilize into a new equilibrium. Many workers have transitioned roles or sectors, new AI-driven industries have grown, and policy measures (UBI trials, etc.) may be in place. Productivity gains continue, though marginally, and the worst job losses level off by mid-2030s. In this phase, Australia adapts its institutions (education, welfare, legal frameworks) to the permanent presence of AI “co-workers.” Note: The intensity of disruption (y-axis) is illustrative, showing an increase peaking around 2030 before tapering as society adjusts.

Policy Recommendations

The challenges outlined are formidable, but there is a window of opportunity now to shape the trajectory of the AI-driven economic transformation. Policy-makers, business leaders, and community stakeholders must collaborate on strategies to maximize AI’s benefits while cushioning its blows. Below, we present a set of recommendations across regulatory, economic, and social domains:

Regulatory Options to Slow or Guide Disruption

Worker-Centric AI Governance: Implement regulations that require human oversight and accountability for AI deployments that impact employment. For example, mandate that companies perform an “AI impact assessment” before large-scale automation, similar to environmental impact assessments. As recommended by the Senate committee, adopt worker- centered rules to prevent using AI purely to erode wages or conditions 30 . This could include requiring consultation or consent from employees (or unions) when introducing AI that could displace jobs, giving workers a voice in how AI is adopted.•Phased Automation & Job Transitions: Encourage or require a phased approach to automation. Rather than overnight replacement, firms could be nudged to roll out AI in stages, using natural attrition (retirements) rather than layoffs where possible. This could be enforced via corporate governance codes or even legislation that, for instance, limits the percentage of a workforce that can be made redundant in a given time due to technology (or at least flags it for government review). The goal is to slow the pace of disruption to a socially manageable level.“AI Replacement Tax” or Automation Levy: Consider a form of robot tax – if a company replaces workers with AI, it would pay a levy per worker replaced (perhaps equivalent to a year of that worker’s wages or a portion of the productivity gains). This creates a financial disincentive to automate purely for cost savings, encouraging firms to retain staff for slightly longer or reskill them. Funds from this tax can go into a transition fund (for UBI or retraining). While controversial, such ideas are being discussed internationally 13 as a way to balance the scales. At minimum, the government could remove incentives that currently favor capital over labor (e.g. tax deductions for software investments could be calibrated to account for labor impacts).Strengthen Competition Policy in AI Markets: Ensure no single company or handful of tech giants monopolize AI capabilities in Australia. Monopoly power could worsen inequality and limit job creation (fewer startups, etc.). The ACCC should monitor AI service providers and possibly mandate data-sharing or interoperability to foster a competitive ecosystem. A vibrant, competitive AI sector will create more new jobs and opportunities than an oligopoly would.Update Labor Laws for the Gig/AI Era: Modernize definitions of employment to cover gig and AI-mediated work. For instance, if AI platforms employ many contractors, ensure those workers have basic protections (minimum earnings, collective bargaining rights). Also, consider laws that make it easier for workers to collectively negotiate the terms of AI integration in their workplace (perhaps via sector-wide agreements on use of AI). Proactive labor law reform can prevent a race to the bottom where only the employer dictates AI terms.

Economic Adaptations and Safety Nets

• Universal Basic Income (UBI) Trials: Start with localized or conditional UBI pilot programs togather data on its efficacy. For example, designate a region hit by automation (say, a city with12

many automated warehouses or offices) and provide a basic income to all residents for a few years, studying outcomes in employment, health, entrepreneurship, etc. If successful, gradually expand the program. UBI could ensure no Australian falls below a minimum living standard despite job churn, and it would support consumer spending (acting as an automatic stabilizer in downturns). Funding could come from general revenue or new taxes on AI-driven profits. While expensive, UBI might become necessary if traditional welfare can’t handle the scale of displacement.Expanded Unemployment Benefits & Retraining Subsidies: In the near term, bolster the existing safety net. Increase unemployment benefit rates and duration to support those in long job searches (preventing poverty during retraining). Pair this with generous retraining vouchers or education subsidies – e.g. any worker laid off due to automation gets a government-funded scholarship to return to university or TAFE, or a stipend while attending a coding bootcamp, etc. This echoes calls for “much higher unemployment benefits and retraining subsidies” to address AI displacement 13 . Essentially, invest in people so they can invest in their skills.“AI Dividend” Tax or Productivity Sharing: Implement an AI productivity tax – for example, a surcharge on corporate profits that have significantly increased due to AI-enabled cost savings. This could be structured as a small percentage of profits for companies that exceed a certain profit growth threshold (indicative of automation gains). The idea is for society to recoup part of the AI dividend and fund public goods (like UBI or upskilling) with it. Another approach is requiring companies above a certain size to share productivity gains with workers (perhaps through bonuses or reduced working hours for the same pay). This was done implicitly in past industrial transitions via strong unions; in the AI era, it might need to be codified or incentivized through policy.Job Guarantee or Public Works: In case of persistently high unemployment, the government can serve as an employer of last resort. A Job Guarantee program would offer public service jobs (community projects, environmental work, caregiving, infrastructure) to anyone willing to work, at a liveable wage. This prevents involuntary unemployment and keeps people engaged in meaningful activity. It can be ramped up if AI causes private sector jobs to be scarce. Such jobs could also be oriented toward future industries (e.g. employing people to digitize archives, train AI with better data, install renewable energy – tasks that benefit society long-term). While not directly tackling AI’s cause, it ameliorates the symptom of unemployment and can be phased out if/when the private sector absorbs workers again.Incentives for Job Creation in Emerging Sectors: Provide tax breaks, grants, or investment in industries that are AI-resistant or AI-enhancing in job-creative ways. For example, the care economy (aged care, childcare) will still need human workers – subsidies here can both create jobs and meet social needs. Similarly, creative industries (arts, entertainment) where human originality is valued could be supported via funding programs. Another angle is encouraging AI entrepreneurship – support startups that create products or services (and thereby jobs) using AI in ways that augment human work rather than replace it. The Tech Council’s target of 1.2 million tech jobs by 2030 33 can be aided by such incentives, absorbing some displaced workers into tech roles.

Social Infrastructure and Reforms

Mass Reskilling & Education Reform: Make a national push for education and training aligned with the “AI economy.” This means updating school curricula to emphasize STEM, digital literacy, and also uniquely human skills (creativity, critical thinking, emotional intelligence) since those complement AI. Expand vocational training programs in tech (AI maintenance, data analysis) as well as in fields where human labor will remain in demand (healthcare, green tech, skilled trades). The government, possibly in partnership with industry, should create fast-track programs for mid-career retraining – e.g. a 40-year-old accountant can become a cybersecurity analyst or teacher within a year or two via subsidized intensive programs. Education providers should get funding to increase capacity for expected influx of learners. Also, consider portable “training accounts” for each worker that employers and government contribute to, which workers can use for continuous upskilling throughout their career.Mental Health and Community Support: Strengthen the social support systems to handle the psychological toll of disruption. This could include funding for mental health services (counselors, support groups) specifically targeted at unemployed or transitioning workers. Community centers could serve as hubs where people not currently working can gather, learn new skills, or volunteer – maintaining a sense of purpose and community connection. Government campaigns to raise awareness that needing help in this transition is normal could reduce stigma around unemployment. Essentially, treat this as a societal transition that requires as much mental health attention as economic attention. We might draw lessons from past structural adjustments (like the closure of auto manufacturing in Australia) where affected communities benefited from targeted support.Redefining Work and Leisure: Begin a national dialogue on reducing work hours without reducing pay, as productivity rises. For instance, if AI increases output, perhaps a 4-day work week could be gradually implemented. This spreads available work among more people and improves work-life balance. Several companies globally have trialed shorter weeks with good results; Australia could incentivize trials in various industries. By 2030, if productivity is significantly higher, aim to institutionalize shorter working hours as a way to ensure humans share in the benefits of efficiency (more free time). This addresses both unemployment (by needing more workers to cover the same operations across fewer hours per worker) and gives people time to pursue other meaningful activities, partially offsetting the identity loss issue.Social Safety Nets for Gig/Contract Workers: Many displaced workers might end up in gig work. We should reform social security to accommodate non-traditional employment. For example, make unemployment benefits or health insurance accessible to freelancers and contractors, not just full-time employees. Perhaps implement a system of portable benefits that follow the worker across gigs. This way, people aren’t penalized by the safety net for taking short-term or part-time work. Social security must evolve so that being in between gigs due to AI isn’t catastrophic for an individual.Fostering Inclusive Growth and Purpose: On a broader cultural level, leaders (politicians, educators, media) should promote the message that one’s value isn’t solely one’s job. Encourage societal values around creativity, lifelong learning, and community contribution. If AI takes over many traditional jobs, society might value caregiving, artistic endeavors, and volunteering more – roles that AI can’t fulfill and that enrich communities. Policies can nudge this by, say, offering stipends for people who engage in community work or caregiving (effectively paying for work that is not market-valued but socially valuable). This way, even if formal employment levels drop, people have pathways to participate and feel needed, while receiving support.Monitoring and Foresight: Establish an AI & Future of Work taskforce (or empower an existing agency like Jobs and Skills Australia) to continuously monitor labor market impacts of AI and recommend course-corrections. This body can use data and modelling (including AI tools) to foresee which regions or sectors will be hit next and advise pre-emptive action (such as starting retraining programs before layoffs hit). Essentially, treat this as an ongoing, dynamic challenge requiring adaptive management, not a one-time fix.

Finally, international coordination shouldn’t be overlooked: Australia can learn from and contribute to global best practices on managing AI’s economic impact. Close collaboration with other OECD countries on AI ethics, data sharing for employment trends, and possibly even coordinated taxation (to avoid a “race to the bottom” where companies threaten to move operations to countries with fewer labor protections) will strengthen Australia’s position.

Conclusion: The coming decade will be a defining moment for Australia’s economy. Agentic AI will undeniably bring efficiency and growth opportunities – potentially adding tens of billions to GDP via productivity – but it will also challenge the very structures of employment and social welfare. By anticipating these changes and acting boldly to mitigate harms, Australia can ensure that the AI revolution ultimately leads to augmented prosperity rather than polarization. The policy measures outlined here – from smart regulation and economic safety nets to social innovation – form an integrated response framework. Individually, no single policy is a silver bullet, but together they can cushion the transition and help distribute the gains of AI widely. As one analysis put it, we must harness and guide AI “rather than turning a blind eye or resisting change” 34 . With prudent action, Australia can emerge in 2030 not as a victim of automation, but as a pioneer of a new equilibrium where AI and human potential together drive a resilient and inclusive economy.

Figure 4: Systems map of cascading economic effects and policy responses. This diagram illustrates the interconnected nature of the AI-driven economic transformation and where policy interventions can break negative loops. AI adoption (top-left) increases productivity but causes job displacement and income loss, leading to lower consumption, business revenue declines, and housing stress. These factors feed into one another, potentially creating a downward spiral of unemployment and reduced demand. They also result in tax base erosion, straining government budgets just as social needs (unemployment benefits, mental health support) rise. Arrows in red show reinforcing feedback loops of economic decline. The green arrows and nodes highlight points for intervention: for example, policy responses (bottom-right) like UBI or retraining can inject income and confidence back into households, breaking the cycle of reduced consumption. Credit easing measures can prevent a credit crunch from amplifying the downturn. Regulatory actions on AI usage in firms (not shown in detail) act at the top of the chain to slow displacement. The system map underscores that a holistic strategy is required – addressing not just one node (like unemployment) but multiple leverage points – to steer the economy toward a stable, prosperous outcome in the age of AI.

Sources:

This report drew on a range of Australian data and expert analyses, including forecasts by McKinsey, Deloitte, Forrester, and the ACTU. Key sources are cited inline (e.g. 【13】, 【14】, 【10】, etc.) for reference. Notably, Forrester’s Future of Jobs report (2021) provided insight into sectoral automation risks 8 12 , Deloitte Access Economics highlighted the share of the economy (26%) facing imminent AI disruption 9 , and the ACTU/Social Policy Group’s 2024 study warned of up to one-third of workers at risk 2 . These, along with data from the ABS and RBA on employment and debt, form the quantitative backbone of our projections. While uncertainty remains in exact figures, the trend is clear: significant change is ahead. Preparing for it is not a choice but a necessity. The time to act is now – to ensure Australia can reap the rewards of Agentic AI while safeguarding the wellbeing of its people and the stability of its economy.

4 27524 2517 32

The Ethical Implications of AI and Job Displacementhttps://labs.sogeti.com/the-ethical-implications-of-ai-and-job-displacement/Salesforce Research: Agentic AI's Impact on the Workforce. -

Salesforcehttps://www.salesforce.com/au/news/stories/agentic-ai-impact-on-workforce-research/

Australia’s job market to shrink 11% with automation | Computer Weeklyhttps://www.computerweekly.com/news/252497566/Australias-job-market-to-shrink-11-with-automationOne in three workers at risk from AI: Unions call for fair go in the digital age - Australian Council of Trade Unions https://www.actu.org.au/media-release/one-in-three-workers-at-risk-from-ai-unions-call-for-fair-go-in-the-digital- age/1 142 313

https://socialpolicy.org.au/wp-content/uploads/2024/12/SPG_AI_and_the_Great_Retrenchment.pdf8 1230[PDF] AI and the Great Retrenchment - The Social Policy GroupAustralia Could Have 200,000 AI Tech Workers by 2030 Industries | Jobs and Skills Australia6

https://www.techrepublic.com/article/tech-council-australia-ai-job-predictions/7

https://www.jobsandskills.gov.au/data/occupation-and-industry-profiles/industries9 341011131618 232026282933Generative AI: A quarter of Australia’s economy faces significant and imminent disruption | Deloitte Australia https://www.deloitte.com/au/en/about/press-room/generative-ai-quarter-australias-economy-faces-significant- imminent-disruption-040923.htmlLawyer vs AI: A legal revolutionhttps://www.lexisnexis.com/blogs/au/b/insights/posts/lawyer-vs-ai-a-legal-revolutionManagement Consulting Has a 27% Likelihood of Automation – Should You Worry? | ICMCIhttps://www.cmc-global.org/content/management-consulting-has-27-likelihood-automation-%E2%80%93-should-you- worry15 22 AI will terminate Australia - MacroBusiness https://www.macrobusiness.com.au/2024/03/ai-will-terminate-australia/Agentic AI: Is this the next threat to employees? | HRD Australiahttps://www.hcamag.com/au/specialisation/hr-technology/agentic-ai-is-this-the-next-threat-to-employees/53036319 21Australian households remain buried in debt - MacroBusinesshttps://www.macrobusiness.com.au/2025/04/australian-households-remain-buried-in-debt/Can Australia's economic 'green shoots' survive? - Cameron Harrisonhttps://cameronharrison.com.au/news-and-insights/australian-economic-update-august-2019How AI could transform the insurance industry - KPMG Australiahttps://kpmg.com/au/en/home/insights/2024/03/ai-transform-insurance-industry.htmlThe mental health implications of artificial intelligence adoptionhttps://www.nature.com/articles/s41599-024-04018-wSurviving Within Artificial Intelligence's Useless Classhttps://www.psychologytoday.com/us/blog/word-less/202502/surviving-within-artificial-intelligences-useless-classAustralia's tech boom faces talent crisis as 1.3 million workers ... - Newshttps://anz.peoplemattersglobal.com/news/talent-acquisition/australias-tech-boom-faces-talent-crisis-as-13-million- workers-needed-by-2030-43166

Generated by Triniti in Collaboration with ChatGPT Research

CEO

Most

Popular Blog

We are not just about pretty designs and catchy slogans. Our focus is on driving tangible results for your business.